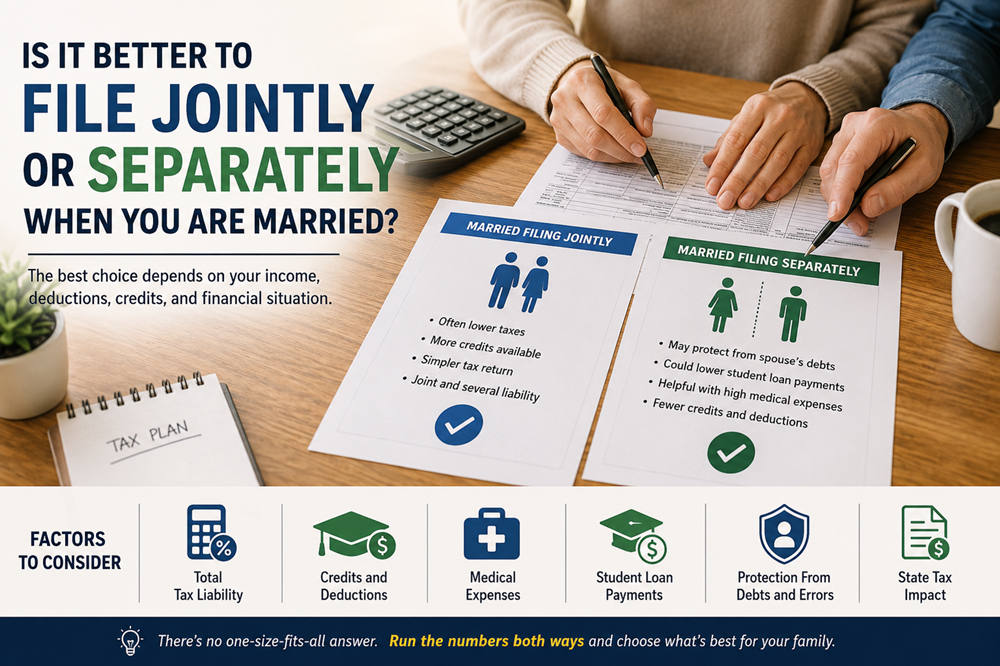

For most married couples, filing taxes jointly results in a lower combined tax bill. Joint filers usually have access to more credits, more favorable tax brackets, and simpler paperwork.

Still, filing jointly is not always the right choice. Separate returns may make sense when one spouse has unreliable tax records, significant medical expenses, federal student loans, or past-due debts. Couples who are separated may also prefer to keep their tax responsibilities apart.

The best choice depends on your complete financial picture—not simply which option produces the larger refund.

What Does Married Filing Jointly Mean?

Married filing jointly means you and your spouse submit one federal tax return. You combine your income, deductions, credits, and tax payments.

Your filing status is generally based on your marital status on the final day of the tax year. Therefore, you can usually file jointly if you were legally married on December 31, even if you lived apart during part of the year.

A joint return can be convenient, but it comes with shared responsibility. Both spouses are generally responsible for the full tax bill, including penalties and interest. This is known as joint and several liability.

That responsibility may apply even when:

- Most of the income belonged to one spouse

- One spouse prepared the return

- One spouse claimed an incorrect deduction

- The couple later divorces

The IRS offers innocent spouse relief in some situations, but approval is not automatic.

What Does Married Filing Separately Mean?

When spouses file separately, each person submits an individual return.

You generally report your own income, deductions, credits, and tax payments. Married filing separately is different from filing as single. Unless you qualify for head-of-household status or another exception, your filing status must still show that you are married.

Separate returns can provide more financial independence, but they often result in fewer tax benefits and more complicated paperwork.

Why Filing Jointly Is Usually Better

You May Pay Less in Combined Taxes

According to the IRS, most married couples save money by filing jointly. Joint tax brackets are generally more favorable, particularly when one spouse earns considerably more than the other.

For example, imagine one spouse earns $100,000 while the other earns $25,000. A joint return applies the married-filing-jointly brackets to their combined income. That may keep more of the higher-earning spouse’s income in lower tax brackets.

The advantage may be smaller when both spouses earn similar amounts, but credits and deductions can still make joint filing more beneficial.

More Tax Benefits Are Available

Married couples filing separately lose access to several popular tax breaks.

Separate filers generally cannot claim:

- The American Opportunity Tax Credit

- The Lifetime Learning Credit

- The student loan interest deduction

The Earned Income Tax Credit and child and dependent care credit are also usually unavailable to married couples filing separately. However, exceptions may apply when spouses lived apart and meet specific requirements involving a qualifying child.

The IRS explains these education-related restrictions in Publication 970. Because the lost benefits can be worth thousands of dollars, couples with children, college expenses, or student loan interest should calculate the difference before choosing separate returns.

Filing Is Usually Simpler

A joint return places both spouses’ information on one set of federal tax forms.

With separate returns, you may need to determine:

- Which spouse can claim each dependent

- Who paid deductible medical or charitable expenses

- How mortgage interest and property taxes should be divided

- How income from jointly owned accounts should be reported

- Whether both spouses must itemize deductions

You may also need to prepare two federal returns and two state returns, increasing both the work and the cost of tax preparation.

Separate Filing Can Restrict Your Deductions

For the 2025 tax year, the standard deduction amounts are:

- $31,500 for married couples filing jointly

- $15,750 for each spouse filing separately

Together, two separate standard deductions equal the joint amount. The problem arises when one spouse itemizes deductions. In that situation, the other spouse generally must itemize too, even when that person has few expenses to deduct.

This can leave one spouse with a much smaller deduction than expected.

When Filing Separately May Make Sense

You Do Not Trust Your Spouse’s Tax Information

Do not sign a joint return containing information you cannot verify.

Filing separately may be safer when your spouse:

- Has unreported business or cash income

- Claims deductions without documentation

- Refuses to share financial records

- Has not filed previous tax returns

- Provides tax information that appears inaccurate

Signing a joint return could make you responsible for additional tax, penalties, and interest if the IRS later discovers errors.

Innocent spouse relief may help in limited circumstances, but filing separately from the beginning can reduce the risk of becoming responsible for a spouse’s inaccurate return.

You Are Separated but Not Divorced

Some separated couples prefer individual returns because they no longer combine their finances.

Depending on your living arrangement, you may qualify to file as head of household instead of married filing separately. You generally must have lived apart from your spouse during the final six months of the year, paid more than half the cost of maintaining your home, and had a qualifying child living with you.

Head-of-household status is usually more favorable than married filing separately. The rules for separated spouses are explained in IRS Publication 504.

One Spouse Has Large Medical Expenses

You can deduct eligible medical and dental expenses only when you itemize. The deduction generally covers the portion of qualified expenses that exceeds 7.5% of adjusted gross income.

Suppose one spouse has a relatively low income but unusually high medical bills. Filing separately may lower that spouse’s adjusted gross income, making it easier to exceed the 7.5% threshold.

However, this does not guarantee savings. You must also consider:

- Which spouse actually paid the expenses

- Whether both spouses will have to itemize

- Which credits will be lost

- The effect on state taxes

The IRS provides a detailed list of qualifying costs in Publication 502. Run the numbers both ways before choosing this strategy.

Filing Separately Could Lower Student Loan Payments

Tax filing status can affect payments under some federal income-driven repayment plans.

Depending on the plan, filing jointly may cause both spouses’ incomes to be included in the payment calculation. Filing separately may allow the calculation to use only the borrower’s income.

Federal student loan repayment rules have changed recently. A March 10, 2026, court order blocked the Department of Education from implementing the SAVE Plan and parts of other income-driven plans. New repayment choices, including the Repayment Assistance Plan, became available beginning July 1, 2026.

Borrowers should review the latest income-driven repayment information and use the federal repayment calculator rather than assuming separate filing will reduce their payments.

Compare the total annual cost of each option:

Taxes when filing jointly + yearly student loan payments

versus:

Taxes when filing separately + yearly student loan payments

A lower monthly loan payment may not be worthwhile if filing separately increases your taxes or eliminates valuable credits.

Your Spouse Owes Past-Due Debts

A joint refund may be used to pay certain debts belonging to one spouse, including:

- Past-due child support

- State income tax obligations

- Federal agency debts

- State unemployment compensation debts

Filing separately may keep your individual refund apart from your spouse’s refund.

You may also be able to file jointly and submit Form 8379, Injured Spouse Allocation. This form asks the IRS to calculate and return the portion of the joint refund belonging to the spouse who was not responsible for the debt.

Injured spouse relief is not the same as innocent spouse relief. Injured spouse relief concerns a refund being used for the other spouse’s debt. Innocent spouse relief concerns unpaid or understated tax on a joint return.

Special Rules for Community Property States

Separate filing can be more complicated if you live in a community property state:

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

State law may treat part of the income earned during the marriage as belonging equally to both spouses. As a result, you may need to report a portion of your spouse’s income even though you are filing separate returns.

IRS Publication 555 explains how community property laws can affect federal returns. Couples in these states may also need to include Form 8958 and follow special rules for dividing wages, investment income, deductions, and tax payments.

Can You Change Your Filing Status Later?

Couples who file separately can generally amend their returns and switch to a joint return within the applicable amendment period.

Changing from a joint return to separate returns is much more difficult. In most cases, you cannot make that change after the original tax-return deadline.

For this reason, compare both options before submitting a joint return, especially when you have concerns about your spouse’s income or deductions.

How to Choose the Better Filing Status

Prepare your return both ways and compare the couple’s total cost.

Review:

- Total federal tax under each option

- Total state tax

- Credits and deductions lost by filing separately

- Federal student loan payments

- Medical-expense deductions

- Tax-preparation costs

- Responsibility for inaccurate tax information

- Whether a refund could be taken for one spouse’s debts

Do not focus only on which return produces the larger refund. A refund mainly reflects how much tax was withheld or paid during the year. The more useful comparison is the couple’s total tax liability and overall financial cost.

Which Filing Status Is Better?

Married filing jointly is usually the better choice. It often produces a lower combined tax bill, preserves more credits, and requires less paperwork.

Filing separately may be worthwhile when you need protection from questionable tax reporting, are separated, have substantial medical expenses, or could significantly reduce student loan payments.

Because the outcome depends on both spouses’ income, deductions, debts, and state tax rules, calculate the return both ways before making a final decision. Complex situations involving self-employment, community property, or disputed financial records may require help from a qualified tax professional.